Is dental insurance worth it?

These days, insurance companies offer coverage for just about any life event imaginable. It isn't always clear which forms of protection are necessary and which are a waste of money.

Take dental insurance. It's no secret that dental work can be expensive, especially for more complicated procedures. Everyone wants a healthy, sparkling smile, which is why many people ask themselves: Should I get dental insurance; do I need dental insurance? Is dental insurance worth it, or is my hard-earned money better spent somewhere else?

Remember that everyone's situation is different. When deciding on a dental benefits plan, it's important to understand how dental insurance works, the factors that determine cost, and what your particular dental needs might be. Estimating costs ahead of time can help you make an informed decision and plan for the year ahead.

Looking for dental benefits? We offer a variety of plans for individuals and families with different coverage options and monthly premiums to fit your needs.

Are Dental Insurance Premiums Worth the Cost?

Many forms of insurance are designed to be a safety net: you pay a premium now so that, in the event of an accident or tragedy later, you're not left with a massive financial burden. It seems like a no-brainer, but when your budget is tight, it can be hard to fork up money for "what if."

Dental insurance works a little differently.

With a dental benefits plan, you don't just protect yourself from catastrophic claims in the future — you try to prevent them from happening at all. Dental insurance is designed to encourage preventive care in order to reduce the risk of costly treatments later. If you make the most out of your dental insurance, it offers tangible benefits and savings both now and in the future. For many people, this difference makes dental insurance worth it.

What Does Dental Insurance Cover?

Although dental benefits can vary widely, the most popular Delta Dental plans provide what's known as 100/80/50 coverage. What these dental benefits cover is broken down like this:

- 100% coverage for preventative care, such as the exams, cleanings, fluoride treatments, and X-rays you receive during regular checkups. These are what help prevent more expensive things like fillings and root canals from being needed in the first place.

- Around 80% coverage for basic procedures such as fillings.

- 50% coverage for major procedures, including crowns, root canals, non-surgical extractions, and gum disease deep cleanings.

Should You Get Dental Insurance?

A common question we hear is "Do I need dental insurance?" And the answer is no. You can certainly go to the dentist without insurance. But the question of whether you should get dental insurance is different altogether.

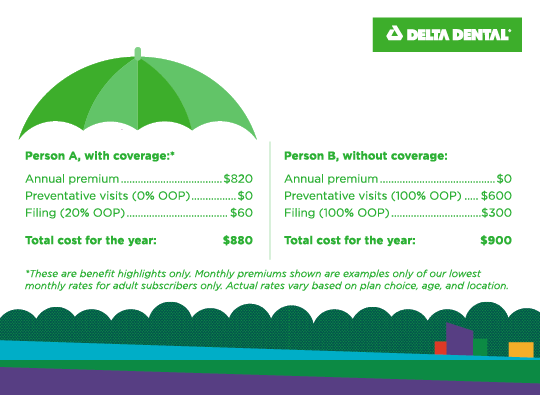

Let's say there are two individuals who both live in Western Washington — all personal factors are the same, except that one has a Delta Dental Premium Plan* (Person A) and one is uninsured (Person B). Let's also say they both go for their twice-yearly preventive visits and each need one cavity filled, but Person B has to pay out-of-pocket (OOP) for all expenses.

Comparing these costs at face value, the difference appears to be negligible. But how many uninsured people are going to the dentist twice a year and paying hundreds of dollars out of pocket each time? Not many.

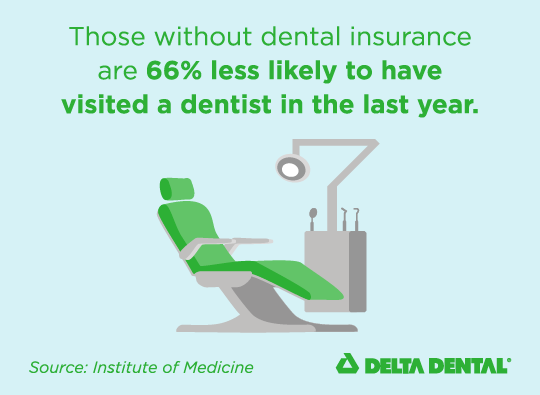

In fact, according to the Institute of Medicine, those without dental insurance are "two-thirds less likely than people with private insurance to have had a dental visit within the last year."

Again, dental insurance is about promoting prevention. Missing preventive dental appointments for long periods of time leads to an increased risk for tooth decay and gum disease. When not addressed in their early and treatable stages, these issues can progress to a point where the only treatment options left are major procedures.

By the time you've reached that point, you could be looking at needing crowns, root canals, extractions, dental implants, and/or deep cleanings that could amount to thousands upon thousands of dollars — all of which could have been avoided.

The Other Health Benefits of Having Dental Insurance

While there are obvious oral health ramifications to missing preventative checkups, these problems can go far beyond the mouth. As we've discussed time and time again, oral health and overall health are strongly connected. Issues that begin in the mouth can work their way into other parts of the body, even contributing to conditions such as diabetes, glaucoma, and heart disease.

So, if you ask us if dental insurance is worth it? We'll give you a resounding yes.