Notice:

How Does Individual Dental Insurance Work?

Dental insurance helps cover the cost of treatments related to the teeth and gums, which in turn helps you maintain a healthy smile. Similar to health insurance, you may have deductibles, co-pays, and coinsurance, and typically, annual maximums — but costs vary from plan to plan.

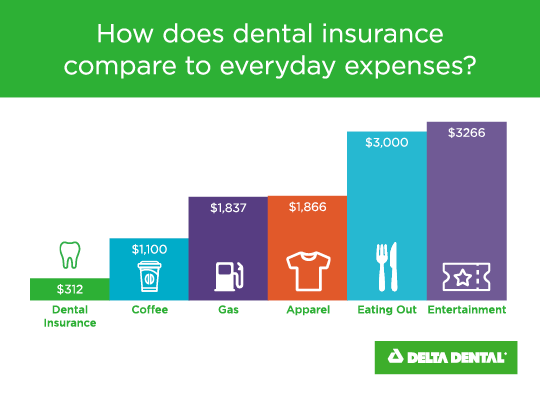

An estimated 74 million Americans don’t have dental insurance coverage, but finding a plan that works for you is easier and more affordable than you think! In fact, the average Delta Dental plan premium ranges from $30-$60 a month – much less than what the average American spends on coffee a month*. Benefits of having dental insurance include:

- Lower costs for non-preventive dental care

- No-cost preventive dental care (like dental exams, cleanings, and x-rays)

- Better overall health — and identification of other problems before they become more serious issues

Looking for dental coverage? Explore our Individual and Family plans to find what’s best for you.

What is dental insurance?

Individual dental insurance is a contract between you and your health benefits carrier. When you enroll in an individual dental plan, you have entered into a contract. This means that you are responsible to pay your premiums and follow the rules of the plan and the carrier — such as Delta Dental of Washington — is responsible to pay your dentist for covered services at agreed upon reimbursement levels.

Dental insurance plans vary so the reimbursement level, or portion that the benefits carrier pays, depends on the plan you choose.

What’s covered by dental insurance?

Dental insurance coverage depends on the plan you choose. Unlike medical insurance, dental insurance plans have a relatively small number of coverage categories, so it’s easy to keep track of what dental services are covered and how much your dental insurance plan pays for each service. If you get familiar with a few key terms, dental insurance coverage is also surprisingly transparent.

What Does Dental Insurance Cover?

Preventive care (also called diagnostic services)

These services and treatments can include cleanings, oral exams, x-rays, fluoride, and sealants. They can also include periodontal (gum) maintenance and deep pocket cleanings.

Restorative and major services

These include fillings, crowns, root canals, extractions, oral surgery and specialty treatments for gum and teeth structures (periodontics), insides of teeth (endodontics), artificial removable teeth (prosthodontics), and braces (orthodontics).

These dental services are reimbursed at different rates and your dental plan document should list each of these services individually, along with the percentage of coverage or the flat fee cost. You will be responsible for the remainder of the cost.

What’s not covered by dental insurance?

Cosmetic dental services, such as teeth whitening or veneers, may not be covered by a dental plan. While some plans do cover orthodontic services, many do not. If you’re interested in having coverage for things like braces to retainers, it’s important to understand the details of the plan you’re shopping for.

Some plans, for example, may cover orthodontic services but may exclude dental coverage for the alignment appliances themselves.

How do I get dental insurance?

If you’re looking to get dental insurance outside of your place of employment, there are a couple of different ways to buy an individual dental plan. How this works depends on the type of coverage you need and how you purchase your insurance.

Health Benefits Exchange:

Many dental insurance carriers offer plans through a health benefits exchange. Washington State, for example, has the Washington Health Benefit Exchange (WAHBE). These plans are designed to meet the needs of families with varying budgets.

Currently, unless you’re over 65 and qualify for Medicare, dental insurance plans can only be purchased through the exchange along with a medical insurance plan.

Standalone plans:

A good number of dental insurance carriers also offer standalone insurance plans. These are purchased directly through the insurance carrier. In this case, you can buy a dental plan even if you have no health insurance.

How do I use my individual dental insurance plan?

- Find a dentist in your network

When you are ready to use your dental insurance plan, it’s important to find a dentist in your plan’s network.

For Delta Dental of Washington, dentists can join two networks. Dentists in the Delta Dental PPO Network often have agreed to accept lower fees than dentists in the Delta Dental Premier® Network. Dentists who choose to not join one of our networks are called Non-Participating Dentists.

With Delta Dental of Washington, you may choose any dentist to provide dental services under almost all of the individual plans. However, your out-of-pocket costs may be substantially higher if you use a Non-Participating Dentist than with a Delta Dental PPO or Delta Dental Premier Dentist. You will be responsible for payment of any balance remaining after the DDWA benefit is paid. -

Verify coverage and benefits

Many dental insurance plans no longer issue physical cards. Instead, if a dentist is in your plan’s network, he or she has a “direct line” to the insurance company. The receptionist or billing specialist can look you up in Delta Dental’s system to verify your coverage and benefits. -

File a dental insurance claim

In order for your dental insurance carrier to pay for your dental bills, you or your dentist have to send in a claim. Usually, your dentist will submit claims for you.

Delta Dental of Washington generally processes all claims within 30 days, unless special circumstances require more time. Once your claim has been processed, you and your dentist will receive a notice to tell you what was paid (called an Explanation of Benefits or EOB). The EOB shows you what the dental insurance carrier has paid on your claim and how the benefits and any copayments or deductibles have been applied.

What are some key terms to know when shopping for dental insurance?

As you shop for coverage, here are a few key terms to further explain dental insurance plans.

Premium: This is the amount you pay each month to be enrolled in a plan. For your plan to remain in effect, you must pay the premium on time.

Deductible: Deductible: The amount of money that you must pay toward the cost of dental treatment before the benefits of the plan go into effect.

Coinsurance: The amount you pay (usually shown as a percentage) toward the cost of your dental treatment after the insurance company has paid their share.

Copay: A flat fee that you pay out-of-pocket for certain dental services. The copay is a predetermined amount and doesn’t change, regardless of how much your dentist charges the insurance company for services.

Annual / Plan-Year Maximum:The total your plan will pay each year for specified dental services.