How Affordable Are Dental Benefits for Small Business

Understanding Costs, Coverage and Options

For many small business owners, offering employee benefits may feel like walking a financial tightrope. Business leaders want to stay competitive, support their employees, and build loyalty — but cost concerns often stop benefits conversations before they begin. Dental benefits are a prime example.

After medical, dental coverage is one of the most popular employee benefits. One study found that 68% of eligible employees enrolled in dental plans when offered. But despite its popularity, dental coverage is frequently assumed to be too expensive or too complex for small businesses to manage.

In reality, data shows that dental insurance is among the most affordable and predictable employee benefits available, especially when compared to medical insurance. According to the Kaiser Family Foundation, medical premiums for individuals can approach $700+ per month while dental premiums are a small fraction of that. Additionally, well-defined annual maximums and lower average deductibles give dental coverage a predictability your team can appreciate.

Understanding how dental benefits are priced — and how different plan models affect cost — can help small businesses make informed, confident decisions that balance budget constraints with employee value.

What Dental Coverage Typically Costs Small Businesses

What Will This Really Cost Per Employee?

Dental benefits are significantly less expensive than many employers expect. For example, internal claims data show that monthly premiums for Delta Dental of Washington’s Patient Essentials Plan may be as low as $42.251. That’s only 5 percent of the average cost of monthly premiums for group medical benefits, according to a KFF employer benefit survey.

The potential costs of not providing dental benefits becomes particularly stark when you consider this report from Wellhub that shows how employee turnover can cost a business as much as 50% to 200% of an employee’s salary due to lost productivity, training, and salary re-leveling.

Dental vs. Health Insurance Costs: Scale Matters

To put dental affordability in context, medical insurance costs for small employers are dramatically higher. According to the Kaiser Family Foundation, the average annual premium for single medical coverage exceeds $8,435 per year, or roughly $702 per month, while family coverage averages nearly $23,968 annually.

Compared to these figures, dental benefits represent a relatively small, predictable investment — one that can deliver outsized value in employee satisfaction and retention, and even positively impact overall health by reducing a portion of your team’s out-of-pocket medical expenses.

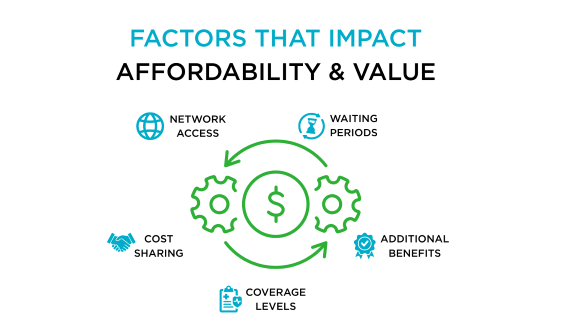

Factors to Consider When Choosing the Right Affordable Dental Plan

Small businesses looking for affordable dental coverage should evaluate more than just the monthly premium. The most cost-effective plans balance affordability with meaningful employee value.

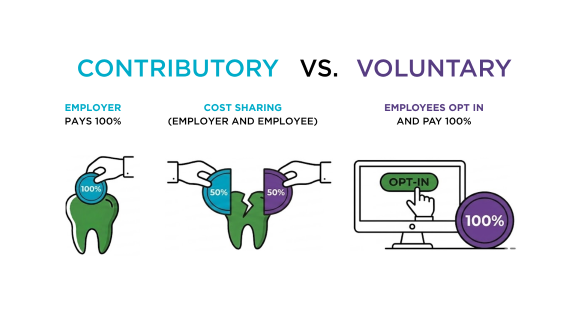

Cost Sharing and Predictability

Small businesses have flexibility in how they structure dental benefits:

- Some employers contribute 50% to 80% of the monthly premium, sharing costs with employees.

- Some employers cover 100% of dental plan costs

- Others offer dental benefits as a voluntary plan, allowing employees to opt in and pay the full premium themselves while still accessing group pricing and provider networks.

Voluntary dental benefits can allow employers to offer coverage with little to no direct financial impact on the business, while still meeting employee demand for dental care access.

Coverage Levels and Annual Maximums

Dental plans generally cover three tiers of care:

- Preventive services: cleanings, exams, x-rays

- Basic services: fillings, extractions, root canals

- Major services: crowns, prosthodontic services, implants

While annual maximums apply, preventive coverage alone can offset a significant portion of an employee’s routine dental expenses.

Network Size and Access

When it comes to the actual value of a dental plan, one of the biggest factors is whether or not an employee on the plan can even see a covered dentist.

Delta Dental of Washington, for example, has the nation’s largest dental network, which means greater access to more in-network dentists with lower pricing in more places.

Access to in-network dentists is a major driver of employee satisfaction. Plans with broader provider networks offer greater flexibility and convenience, particularly for employees who already have established dental providers.

Understanding what kind of network is important too, though. You’ll find that some networks are leased (ex: Delta Dental’s networks are not leased), while others are managed directly by the plan administrator. If a network is leased, it may look like a large network but the plan administrator has less control over the costs of care. Meanwhile, a direct-managed network is a network of providers who negotiate directly with the plan administrator to keep costs as low and as predictable as possible.

Waiting Periods

Some plans impose waiting periods for major services, which may matter depending on employee needs. For example, some plans that offer higher coverage for orthodontia or complex procedures require the enrollee to carry the plan for a period before they are eligible to be covered for the care.

Fortunately, Delta Dental of Washington’s dental plans for small businesses do not have waiting periods, making it easier for employees to access dental services.

What Employers Should Know Before Choosing Dental Coverage

True affordability is defined by the upfront cost and the value, predictability, and simplicity of the product. Before selecting a dental plan, small businesses should take a holistic approach:

- Assess employee needs, including how many employees regularly seek preventive care

- Define budget boundaries and contribution preferences

- Consider company culture, such as whether employees value choice or simplicity

- Evaluate administration requirements, especially for small or multi-role HR teams

Working with a knowledgeable benefits partner can help small businesses compare options efficiently and align plan design with budget and workforce goals. And benefit partners often are a great resource to chat through these questions. For example, Delta Dental of Washington has a team of representatives ready to help you every step of the way.

Bottom Line

The true affordability of dental benefits lies in their low relative cost, predictable pricing, and high employee value. For small businesses navigating rising benefit expenses, dental coverage offers one of the clearest opportunities to support employee health, improve retention, and remain competitive — without overextending financial resources.

When evaluated with the right data and decision framework, dental benefits are often not only affordable — they’re one of the smartest benefit investments a small business can make.

1 This rate is for employee only coverage, $1,000 annual maximum, $50 deductible in Eastern Washington.